Inventory is often the largest current asset on a company’s balance sheet. However, many business owners and financial managers view it simply as products sitting on a shelf. In reality, inventory represents “unliquidated cash.” How you track, value, and report that cash can significantly impact your company’s tax liability, net income, and overall financial health.

Inventory accounting is the body of accounting that deals with valuing and accounting for changes in inventoried assets. It follows specific regulatory frameworks, such as GAAP (Generally Accepted Accounting Principles) or IFRS (International Financial Reporting Standards), to ensure that a company’s financial statements accurately reflect the cost of goods sold and the value of remaining stock.

What is Inventory Accounting?

At its core, inventory accounting focuses on assigning a precise monetary value to items in stock. This isn’t just about counting units; it’s about tracking the costs associated with acquiring that inventory and moving it through the production or sales cycle. Because prices for raw materials and shipping fluctuate constantly, the “cost” of an item bought in January might differ from one bought in June.

To maintain an accurate record, businesses must establish a beginning inventory the total value of all goods a company has in stock at the start of an accounting period. This figure is crucial because it serves as the baseline for calculating the cost of goods available for sale. If your opening figures are inaccurate, your entire financial reporting for the quarter or year will be skewed.

Why It Matters for Your Business Growth

For a growing enterprise, inventory accounting is more than just a compliance task. It provides the data needed to make informed strategic decisions. Without precise accounting, a business might face:

- Profit Miscalculation: If you undervalue your stock, your profits may appear lower than they actually are, potentially hurting your ability to secure loans or investment.

- Tax Inefficiencies: Overvaluing stock can lead to higher reported profits, resulting in a larger tax bill than necessary.

- Cash Flow Bottlenecks: Poor tracking leads to overstocking (tying up cash) or understocking (losing sales).

By treating inventory as a dynamic financial asset rather than static physical items, companies can optimize their supply chain and improve their bottom line. Understanding the movement from your initial stock levels to your final sales is the first step in achieving operational excellence.

The Three Main Types of Inventory: Tracking the Lifecycle of Goods

![]()

In corporate finance, inventory is not a single category. Businesses must track assets based on their production stage. This helps accountants see where cash is tied up. It also reveals if the factory floor is moving efficiently.

Most businesses divide their stock into three distinct groups:

1. Raw Materials

These are the basic items used to create a product. For a furniture maker, this includes wood and fabric. For a tech firm, it means chips and plastic. Tracking raw materials is vital. Their prices change quickly due to global supply chain shifts.

2. Work-in-Process (WIP)

WIP refers to items currently on the production line. These are no longer just raw materials. However, they are not yet finished products. This category includes the cost of materials and labor. It also includes factory overhead, like electricity. High WIP levels can signal a bottleneck in your process.

3. Finished Goods Inventory

Once a product passes all quality tests, it becomes Finished Goods Inventory. This is the final stage before a sale.

This category represents the total cost of production. It includes everything from materials to final labor. Managers must monitor this closely. If this stock is too high, sales may be lagging. If it is too low, you risk losing customers to competitors.

Why Categorization Matters for Your Balance Sheet

Each stage carries different financial risks. Raw materials are easy to value. In contrast, WIP is harder to value because the items are incomplete.

By separating these types, a company can apply valuation more accurately. It helps the finance team find “dead stock.” This refers to items that no longer move or sell. It also helps manage carrying costs in specific areas.

A professional balance sheet shows the sum of these three parts. Understanding this flow is essential for any manager. It ensures your records match the physical reality of your warehouse.

Inventory Valuation Methods: Choosing the Right Approach

Businesses must choose a specific method to value their stock. This choice affects both taxes and reported profits. Prices usually change over time. Therefore, the “cost” of an item depends on which accounting method you use. There are three primary ways to handle this.

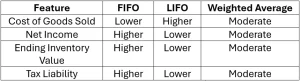

First-In, First-Out (FIFO)

The FIFO method assumes that the oldest items in your warehouse are sold first. This is a very common approach because it follows the natural flow of most goods. For example, a grocery store sells the oldest milk before the new delivery.

In a period of rising prices, this method results in a higher net income. This happens because you are recording the sale of older, cheaper items against current revenue. Consequently, your remaining stock on the balance sheet reflects modern, higher prices.

Last-In, First-Out (LIFO)

LIFO is the opposite of the previous method. It assumes the most recently purchased items are sold first. While this rarely matches physical flow, it offers tax advantages. During inflation, LIFO records higher costs for goods sold. This reduces taxable income, which helps companies save on tax payments. However, many international standards, like IFRS, do not allow this method.

Weighted Average Cost (WAC)

This method provides a middle ground. It does not track which specific item was sold. Instead, it takes the total cost of all items and divides it by the total number of units. This creates a “smooth” average price. It is ideal for businesses with high volumes of identical items, such as fuel or grains.

Comparison of Valuation Impacts

Choosing a method is a strategic decision. Below is a quick look at how these methods perform when prices are rising:

Key Formulas & Metrics You Need to Track

Numbers tell the story of your business health. In inventory accounting, formulas help you translate physical items into financial data. These metrics allow you to measure efficiency and profitability.

Here are the essential calculations every manager should know:

1. Cost of Goods Sold (COGS)

COGS is the most important figure in your inventory report. It represents the direct costs of producing the goods sold by a company. This includes the cost of the materials and the labor used to create the product.

To find this, you need to know your ending inventory. This is the total value of products remaining on hand at the end of an accounting period. The formula is simple:

If your COGS is too high, your gross profit will drop. Tracking this helps you decide if you need to find cheaper suppliers.

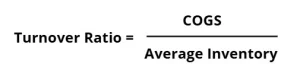

2. Inventory Turnover Ratio

This metric shows how many times a company has sold and replaced its stock during a specific period. A high ratio usually means strong sales. A low ratio might mean you have too much excess stock.

To calculate this, you first need to find your average inventory. This is the median value of your stock over a specific time. You calculate it by adding the beginning and ending stock levels and dividing by two:

Once you have that, use this formula:

3. Days Sales in Inventory (DSI)

DSI tells you how many days it takes to turn your inventory into sales. A lower DSI is generally better. It means your cash is not tied up in products for very long. This liquidity is vital for paying bills and investing in growth.

Common Challenges in Modern Inventory Accounting

Maintaining accurate records is difficult in a fast-moving market. Many businesses struggle with discrepancies between their digital ledgers and physical reality. Even small errors can lead to major financial losses over time.

Here are the most common obstacles faced by modern companies:

1. Inventory Shrinkage

Shrinkage occurs when the physical stock is less than the amount recorded in the books. This usually happens due to theft, damage, or administrative errors. If you do not track this closely, your assets will be overvalued. Professional accounting requires regular physical counts to reconcile these differences.

2. Ghost Assets and Obsolete Stock

Sometimes, items remain on the books even though they are no longer sellable. This is known as obsolete stock. It often happens in industries with fast-changing trends, like fashion or tech. Keeping these “ghost assets” on your balance sheet inflates your company’s value artificially. It also leads to higher insurance costs and storage fees.

3. Supply Chain Volatility

Global events can cause the price of goods to spike or drop suddenly. This makes valuation a moving target. If you use a manual system, catching these price changes is nearly impossible. This volatility often leads to inaccurate COGS calculations and poor tax planning.

4. Human Error in Data Entry

Manual data entry is a major risk factor. One misplaced decimal point can change your profit reports by thousands of dollars. This is why many firms are moving away from spreadsheets. They are looking for more reliable ways to ensure data integrity.

Strategic Implementation & Technology

Modern business moves too fast for paper ledgers. To stay competitive, companies must bridge the gap between accounting and technology. Strategic stock management is no longer just about counting items. It is about using data to drive growth.

Here is how successful firms modernize their inventory accounting:

Digital Transformation and Automation

Many businesses now use automated systems to track every movement of goods. These systems link directly to the accounting software. When a barcode is scanned, the ledger updates instantly. This eliminates human error and provides a real-time view of your current assets. Automation ensures that your valuation—whether using FIFO or Average Cost is always precise.

Implementing Best Practices

Relying on software is not enough. You must also follow Best Practices for Successful Stock Management. These include:

- Regular Audits: Conduct “cycle counts” instead of waiting for a yearly inventory. This keeps your books accurate year-round.

- Safety Stock Levels: Set clear triggers for when to reorder. This prevents stockouts without over-investing in excess items.

- Supplier Relationship Management: Work closely with vendors to understand lead times. This reduces the risk of sudden price spikes affecting your COGS.

The Role of Integration

The best accounting strategy integrates your warehouse data with your financial reports. When your sales team, warehouse staff, and accountants see the same data, the business runs smoothly. This transparency is vital for meeting E-E-A-T standards. It shows that your business operates with high integrity and professional oversight.

FAQ

What is the difference between Periodic and Perpetual inventory systems?

A periodic system updates inventory records at specific intervals, usually through a physical count. In contrast, a perpetual system updates records in real-time after every sale or purchase. Modern businesses prefer the perpetual system because it provides more accurate and up-to-date financial data for decision-making.

How does inventory valuation affect my company’s taxes?

Valuation methods directly impact your Cost of Goods Sold (COGS). For example, during inflation, the LIFO method results in a higher COGS and lower taxable income. This can reduce your tax bill. Conversely, FIFO often leads to higher reported profits and higher taxes. Always consult with a tax professional before choosing a method.

What is inventory shrinkage, and how do I account for it?

Inventory shrinkage is the loss of products between the point of manufacture or purchase and the point of sale. Common causes include theft, damage, or administrative errors. To account for it, you must perform a physical count and then adjust your ledger to match the actual stock on hand. This adjustment is typically recorded as an expense.

Conclusion

Inventory accounting is the heartbeat of any product-based business. It transforms physical stock into actionable financial intelligence. By mastering valuation methods and tracking key metrics like COGS, you protect your company’s profit margins and ensure tax compliance. As your business scales, managing these assets manually becomes a risk to your accuracy and growth. Professional accounting ensures that your balance sheet reflects the true value of your enterprise, providing the transparency needed for stakeholders and future investments.

To eliminate errors and gain real-time visibility into your stock, you need a robust digital solution. Transitioning from spreadsheets to an automated system is the best way to maintain a competitive edge. Streamline your operations and ensure total financial accuracy with TAG Samurai Inventory Management. Our platform simplifies complex accounting tasks, tracks every item in real-time, and helps you implement the best practices discussed in this guide. Take control of your assets today and turn your inventory into a powerful engine for cash flow.